Ensuring that Canadians can comfortably afford their mortgages is a prudent policy goal, since its aim is to protect homeowners and the broader economy from undue risk. However, Canada’s mortgage rules have gone too far, and the mortgage stress test is particularly problematic. By overtightening in the name of safeguarding financial stability, restrictive mortgage rules are increasingly locking well-qualified buyers out of homeownership at a time when entering the housing market is already extraordinarily difficult. This, in turn, is having an adverse impact on the creation of new housing supply for ownership.

The stress test needs to be fixed to reflect today’s realities.

What is the mortgage stress test?

The prescribed minimum qualifying rate (MQR), known as the mortgage “stress test,” is a federal rule that requires borrowers to prove they can afford their mortgage payments at a benchmark interest rate of 5.25% or 2% above the rate they will actually pay (whichever is higher). Its purpose is to ensure households can continue to service their mortgage if interest rates rise or their financial situation changes.

Who regulates the mortgage stress test?

Introduced in 2016 due to concerns about home price growth and household debt levels, the mortgage stress test is governed and implemented by two federal entities:

- The Office of the Superintendent of Financial Institutions (OSFI) – Canada’s banking regulator – sets the stress test rules for uninsured mortgages (i.e., those with a down payment of 20 percent or more), and

- The Department of Finance sets the stress test rules for insured mortgages (i.e., those with a down payment of less than 20 percent), which are backed by the Canada Mortgage and Housing Corporation (CMHC) or private mortgage insurers (Sagen and Canada Guaranty).

While provinces regulate credit unions and some other lenders, many adopt the stress test there as well, and thus the stress test applies broadly across Canada’s mortgage market.

How the stress test is locking well-qualified buyers out of homeownership

While well-intentioned, the mortgage stress test has become so restrictive that it has had an adverse impact on well-qualified buyers’ ability to access homeownership.

For example, since most contractual mortgage rates are currently higher than 4%, the “contract rate plus 2%” usually applies, sometimes testing borrowers in the 7% to 8% range. This means that even if a borrower can comfortably afford their actual mortgage payments at today’s higher mortgage rates, they may still be denied if they cannot qualify at the still higher, hypothetical rate, even if they’re locked into fixed terms where the rate will not change. What’s more is that their income will more often be higher at renewal time, while interest rates are likely to stay the same or come down.

This overtightening has contributed to rapidly falling homeownership rates over the years. According to the 2021 Census, Canada’s homeownership rate dropped 2.5% between 2011 and 2021. That translates to roughly one million more Canadians renting instead of owning homes they can reasonably afford. Given that Canada’s housing affordability challenges persist, that figure is likely higher today.

This decline is not the result of reckless borrowing being curtailed. Rather, it reflects how increasingly restrictive mortgage rules are preventing capable buyers from qualifying, even when they have stable incomes, strong credit histories, a track record of responsible financial management, and growing household incomes ahead.

It’s clear that this disconnect between policy assumptions and real-world affordability is pushing homeownership further out of reach for some well-qualified buyers.

Mortgage risk is at historic lows

Many justify the stress test because of the avoided mortgage delinquencies and stronger financial sector. But a look at the data tells a more nuanced and important story that calls for policy change.

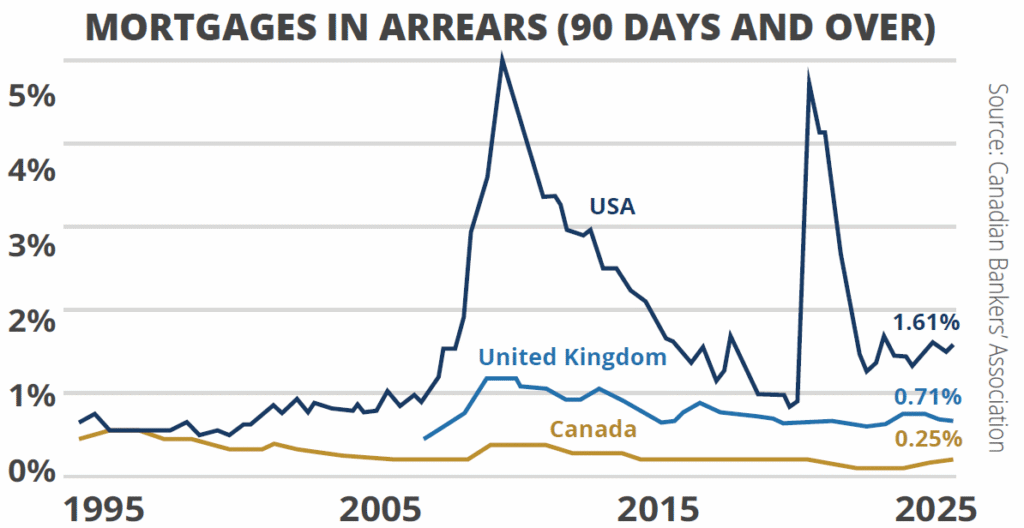

Mortgage arrears (i.e., missed mortgage payments of 90 days and over) in Canada are at near record lows, and remain one of the lowest among the world’s most advanced economies. As of today, Canada’s arrears rate sits at just 0.25%, well below the historical average of 0.33%, and six times less than the current U.S. arrears rate of 1.61%.

What’s more is that Canada’s mortgage arrears rate has stayed low through difficult financial times in recent years. Challenging times mean that arrears should rise, at least a little, and there are many mechanisms for financial institutions to help homeowners when such times arise. But when arrears rates barely rise at all, it means regulations have overcompensated – the cost being thousands of buyers who could and should have qualified for a mortgage (and who would not be in arrears) have instead been locked out of homeownership. The data shows that more than 99.7% of mortgage holders at a bank are not overextended and therefore are not delinquent. Moreover, that number has barely changed when it should have risen to a degree. Instead, hundreds of thousands of households have been prevented from becoming homeowners.

Canadians are demonstrating exceptional discipline when it comes to servicing their mortgage debt, even in the face of higher interest rates and broader economic uncertainty. Meanwhile, thousands who could do the same have been locked out of homeownership. Excessive mortgage over-tightening should be adjusted to be more balanced.

Mortgage debt is not consumer debt

Critics against changes to the stress test tend to view mortgage debt the same way as consumer debt. That argument fails to recognize that mortgage debt is fundamentally different from consumer debt. It finances an appreciating, productive asset, rather than discretionary consumption.

Lumping mortgage borrowing into the same risk framework as consumer debt ignores this distinction and leads to overly cautious rules that do not reflect actual borrower behaviour or outcomes. The data shows that Canadians are in strong financial shape when it comes to their mortgages. Reasonable safeguards will always be necessary, but policy must be grounded by evidence. It’s clear that today’s mortgage stress test is no longer proportionate to the risk it’s meant to address.

Why this impacts the creation of new housing for ownership

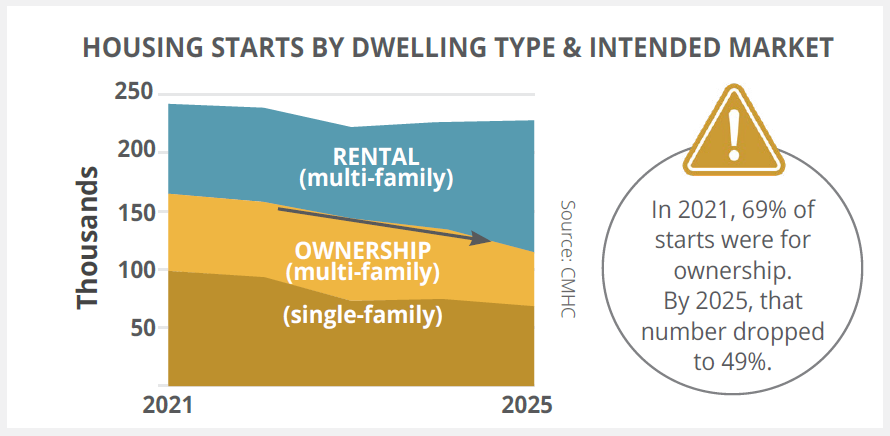

The reduced access to homeownership, particularly for first-time and move-up buyers who could otherwise afford their homes, is having an adverse impact on the creation of new housing supply for ownership at a time when it is desperately needed.

In fact, in 2021, 69% of housing starts were for ownership. By 2025, only 49% were ownership, with the rest being for rental.

Yet, new data from Abacus Data shows that 88% of Canadians under 45 would like to own a home if they could. CMHC also advises that if Canada is to overcome the housing deficit that is contributing to the affordability crisis, 75% of the new supply built must come in the form of housing for ownership. Overly restrictive mortgage rules not only put the homeownership aspirations of Canadians farther out of reach, but they also contribute to the shortage of homes for ownership, which only drives up home prices even further.

CHBA recommendations for fixing overly tight mortgage rules

It’s clear overly restrictive mortgage rules like the stress test are impacting Canadians’ ability to buy homes that meet their needs, and, in turn, slowing the creation of new housing supply.

CHBA recognizes this challenge and has the following recommendations for the federal government to improve how mortgage rules are implemented, including:

- Imploring OSFI to eliminate the stress test on uninsured mortgages.

- Making the stress test for insured mortgages dynamic (including following through on the federal commitment to review this stress test, which is the domain of the government, not OSFI).

- Directing OSFI to avoid further changes to its B-20 guidelines that make it even harder to qualify for a mortgage.

- Adjusting the Interest Act to facilitate 7- and 10-year mortgages and removing the stress test on them.

Housing affordability and the supply of homes for ownership are under severe strain, and Canada needs mortgage rules that strike a better balance. The bottom line is simple: Canadians have proven that they can manage their mortgages. It’s time for mortgage policy to better reflect that reality. Protecting Canada’s financial system must recognize that responsible homeownership is part of the solution, not the problem.

For more of CHBA’s recommendations on how the federal government can help solve the housing supply and affordability crisis, visit How the government can help unlock the door to homeownership.