Housing affordability affects us all. Whether you want to buy your first home, or you’re struggling to pay rent, or you want your children to be able to live in the same area they grew up in – but are currently priced out of – housing affordability affects you.

The federal government has recognized that Canada is in a housing crisis. CMHC estimates that 4.8 million homes are needed over the next decade, which would mean nearly doubling Canada’s housing starts to between 430,000 to 480,000 per year.

So if we need more homes, why are housing starts for homeownership falling? And why is industry currently laying off thousands of people, which is putting Canada at risk for permanent labour capacity loss to build the houses we need in the future? The answer is that housing affordability for the average Canadian is getting worse.

Canadians still very much want to own a home. According to a 2025 public opinion poll by Abacus Data for the Canadian Home Builders’ Association, 88% of Canadians under 45 would like to own a home one day. But sadly, only 29% of non-homeowners are confident they’ll ever be able to buy a home.

Fewer than one in five Canadians think that any level of government is doing enough to address housing affordability for homeownership. When asked which level of government is most responsible for solving the housing crisis, two thirds pointed to the federal government.

Lately, the federal government has been focused on Build Canada Homes, which is a plan to build social housing principally on federal lands. This is important work, but Build Canada Homes will only create about 1% of the new construction that is needed… and it won’t support market-rate housing, which is what 95% of Canadians live in. Canadians view non-market housing as important (and it is) so while they support non-market housing initiatives, their #1 concern is affordability for the homes they hope to buy. So it makes sense that only 17% of Canadians think the federal government is doing enough to address affordability for homeownership.

The Role of Government

All levels of government have a role to play. Governments remove barriers to more housing supply and avoid adding costs to housing, so that prospective home buyers have reasonable access to homeownership, and so those who rent do so because it’s truly their best option based on affordability and preference.

Remember that housing is a continuum, and that ensuring a healthy market for the 4 in 5 Canadian renters who want to buy a home frees up space and resources for Canadians who truly need rental options. The federal government can play a key role by supporting policies that will improve housing affordability and, in turn, foster an environment conducive to increasing housing supply for ownership.

Policies that will improve housing affordability and, in turn, increase supply

So what measures can improve housing affordability? Solutions will come in the form of measures to improve housing supply so that demand doesn’t keep driving up prices, which will take a immediate return to federal leadership with a comprehensive approach to market-rate housing. They’ll come from lowering taxes on new homes, which make up more than 30% of the price of a new home in some municipalities. They’ll come from fixing the stress test and implementing smarter mortgage rules that address risks without locking too many Canadians out of homeownership, especially first-time buyers. They’ll come from removing barriers within the home building process that are making it harder and more expensive to build homes. And they’ll come from supporting the residential construction industry to help keep it building and renovating—from supporting the workforce through immigration and training, to investing in increased productivity in the sector.

At the Canadian Home Builders’ Association, we know how housing in Canada works, and the policy changes it will take to make it less expensive and faster to deliver housing. We strive to ensure Canadians have access to the homes that meet their needs at a price they can afford. A healthy housing market is good for this key industry that creates so many jobs, yes. But more importantly, it’s good for Canadians, and it’s why we’re passionate.

The following policies can unlock the door to homeownership and improve housing affordability:

1. RETURN TO FEDERAL LEADERSHIP AND A COMPREHENSIVE APPROACH TO AFFORDABILITY FOR MARKET-RATE HOUSING… NOW

Canada is still experiencing a housing supply crisis, and homeownership rates are falling.

We need more of the right kind of housing, in the right places. When there isn’t enough supply of the types of homes that people want to buy, house prices go up by too much, and too quickly. The government’s analysis and setting the goal to double housing production was very helpful Budget 2023 and 2024, and Canada’s Housing Plan (2024), contained significant focus and measures to advance affordability for market-rate housing.

Since then, the federal government has shifted its attention away from housing affordability for middle-income Canadians. Support for non-market housing is important, but it should not come at the expense of measures to improve market-rate housing affordability; both can be improved. According to an Abacus Data study for CHBA in 2025, 67% of Canadians say the federal government should be putting more focus on homeownership affordability. When you drill down into the data, 31% say “much more” focus should be placed on it, compared to 17% for non-market housing.

It’s time for the government to re-focus on measures to support average Canadians and homeownership.

Action now is critical given the trade war, which is hampering consumer confidence and resulting in fewer home purchases, leading to fewer housing starts. Renovation, which also creates new supply, has slowed as well. As a result, according to CHBA’s Housing Market Index survey, over 40% of CHBA members are laying off workers, risking permanent labour capacity loss, since many of these workers will move on to other sectors and not return. This will make doubling housing starts in the future nearly impossible. To turn the tide, it’s essential that the government move swiftly.

The federal government is uniquely positioned to lead on market-rate housing affordability, even though all levels of government have an important role to play. Canadians expect this, and are currently not satisfied with any level of government on housing affordability.

Recommendations:

- This government needs to immediately return to that focus on market-rate affordability in a comprehensive fashion, especially when it comes to homeownership.

- The federal government also needs to continue to lead collaboration with provincial and municipal levels of government to use all levers to improve housing affordability and increase housing supply, especially for ownership.

2. LOWER TAXES TO ADDRESS AFFORDABILITY AND GET THE MARKET MOVING

Government taxes and fees are a major contributor to high house prices. In some municipalities, they make up more than 30 percent of the price of a new home.

GST Relief

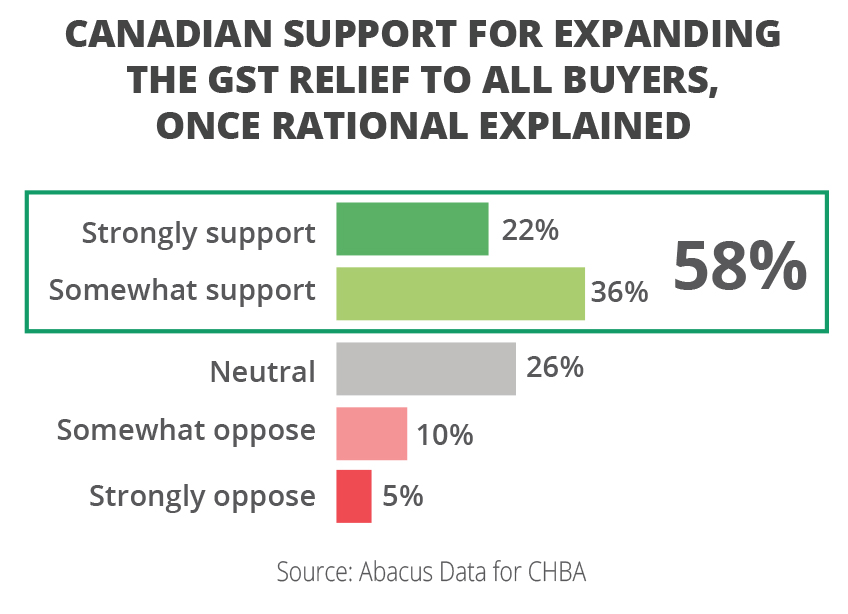

Supporting first-time buyers by removing GST on new homes is a start, but according to the Parliamentary Budget Officer, first-time buyers make up only 5.8% of buyers of new homes. The relief needs to be extended to all buyers.

Expanding the rebate would encourage more “move-up” housing – helping families move from starter homes into larger homes, which frees up starter homes for others. It would also help older adults downsize into newly-built homes, creating more supply and releasing family-sized homes back into the market.

GST relief should also be extended to the creation of accessory dwelling units (ADUs) and renovations that create secondary suites to create more infill housing supply. These housing types have the added benefit of supporting seniors looking to age in place, students, lower income workers, and more. (Read more on this page).

The Abacus research showed that once the rational is explained to them, 58% of Canadians support expanding the GST relief to all buyers, while only 15% oppose.

Recommendations:

- Broaden the GST relief to all buyers of new construction homes.

- Make the GST relief applicable to renovations that add an additional unit of housing to existing homes, like Accessory Dwelling Units (ADUs) and secondary suites.

Addressing Development Taxes

Development taxes (development charges, lot levies, amenity fees, etc.) have risen over 700% over the past 25 years. They add nearly $200k on a typical home in the GTA and nearly $100k in the GVA, deeply impacting housing affordability and supply. Many of the items these taxes fund should be spread across the entire tax base and funded across the longer life expectancy of the infrastructure at the lower rates that municipalities can get, rather than on 25-year mortgages at much higher rates.

The federal government should use all its levers to assist municipalities in reducing their development taxes (which are ultimately paid by homebuyers) by increasing housing-supportive infrastructure and transit investments and tying them to housing supply outcomes.

Recommendations:

- Continue pressure through all means to have municipalities reduce development taxes (e.g. through requirements in funding transfers for infrastructure and transit; and through the Housing Accelerator Fund).

- Follow through on commitments to offset development charges with federal funding (and provincial funding).

- Given that many municipalities have come to rely excessively on development taxes, work with provinces and municipalities to mandate that alternatives to development taxes be found and used instead. Examples of alternative solutions include:

- Municipal debt financing, including shifting some charges to property taxes, particularly for services that benefit the wider community (beyond the new development) such as libraries, roads, and new fire stations.

- Implementing user charges for certain services (e.g. water and wastewater).

- Adopting land value capture techniques for transit improvements.

- Community development districts / municipal service corporations.

- Updating provincial development tax legislation.

3. FIX THE STRESS TEST

There are three factors that determine housing affordability: the person’s income, the mortgage rules in play, and the price of the home. Wages have not kept up with today’s high home prices and interest rates, and first-time buyers are inordinately affected by mortgage rules, especially those seeking insured mortgages, yet they are the lowest-risk group of buyers. They’re also the financial future of Canada. They’re starting their careers and their salaries are just beginning to grow, which also lowers risk at mortgage renewal time down the road.

Rising mortgage rates and ever-tightening mortgage rules have made access to homeownership for first-time buyers more and more difficult. If they’re not buying homes, it reduces the industry’s ability to build more homes. When housing starts for ownership slow, it doesn’t mean that the demand for more homes has gone down, but rather that it’s been artificially repressed by policy. And when young people and new Canadians who want to own homes can’t move out of rental units, it puts more pressure on the rental market, driving up rental prices. A healthy housing continuum includes robust market rate housing options, and diverse pathways to homeownership, supported by sound mortgage policies.

Mortgage rules have been so tightened that homeownership rates have been falling severely since 2011. This has been done in the name of financial sector stability, yet mortgage arrears of 0.25% continue to be at near historic lows, well below their long-term average of 0.33% (Canadian Bankers Association), and 6 times less than the current US rates of 1.61%.

That means more than 99% of mortgage holders at a bank in Canada are not delinquent, and Canada’s arrears (90 days and over) rate remains one of the lowest among advanced economies.

The cost of over-tightening mortgage rules has been a severe drop in homeownership rates, with a 2.5% drop since 2011 (likely more by now), equating to 1 million more Canadians now renting instead of owning.

With the bond market still elevated, 5-year mortgage rates are dropping much less than the Bank of Canada rate, making more mortgage reform as important as ever. Meanwhile, the excessive stress test continues locking out thousands of well-qualified buyers.

We need to help young people overcome today’s obstacles to homeownership. And since one of the biggest obstacles – high home prices – is caused by a lack of supply, the key issue of housing supply should be considered in all monetary and regulatory policy (e.g. any actions by the Bank of Canada, Finance/CMHC, and OSFI).

Recommendations:

- Eliminate the stress test on uninsured mortgages (OSFI). Make the stress test dynamic for insured mortgages (including following through on the federal government commitment to review it).

- Direct OSFI to avoid further changes to OSFI B-20 guidelines that make it even harder to qualify for a mortgage.

- Adjust the Interest Act to facilitate 7- and 10-year mortgages and remove the stress test on them.

4. FUND HOUSING-SUPPORTIVE INFRASTRUCTURE

More housing cannot be built without the infrastructure required to service it. When requiring municipalities to reduce development taxes, making up some of that difference with federal funds is appropriate and important (and this should not be restricted to those municipalities that have excessively raised development taxes and are now struggling – providing infrastructure funding to municipalities that have avoided high development taxes is important too).

Recommendation:

- Maintain and increase housing-supportive infrastructure and transit investments and tie them to housing affordability and supply outcomes (e.g. requirements to lower development taxes, increase density, reduce parking requirements, etc.).

5. REMOVE MUNICIPAL BARRIERS AND RED TAPE WITHIN THE HOME BUILDING PROCESS

Barriers within the home building process result in delays that make building more homes more difficult and costly, which in turn impacts housing affordability and the industry’s ability to build more homes. All levels of government should be trying to remove barriers within the home building process in order to facilitate increasing Canada’s housing stock.

The government should keep working with municipalities to get more homes built. It should also make sure its own actions do not make homes even more difficult to build by fixing unnecessary federal red tape that are making homes more expensive and placing an extra unnecessary burden on home builders.

While there is a good drive to reduce inter-provincial trade barriers, the current system has created inter-municipal trade barriers for housing productivity through overzealous and inconsistent regulation in different municipalities and even within the same municipality.

Recommendations:

- Continue to work with municipalities to support and/or require (tied to funding) municipal process improvements (e.g. zoning, bylaws, approval/permitting delays, NIMBYism).

- Work with provinces to harmonize all municipal building and development-related regulations to eliminate differences in building regulations and code interpretations that prevent the rapid deployment of housing.

5. AVOID ADDING COSTS THROUGH CODES AND REGULATIONS

Many new policy directions that put pressures for more stringent codes and regulations (e.g. climate change mitigation, resiliency, accessibility and others) are put in place with good intention, but can be very expensive, and can often be excessive. In many cases, voluntary measures would be much better. Unfortunately, almost all short-term actions to address these policy priorities through mandatory regulation increase costs to housing. It is critical to innovate and find solutions to these challenges without driving up housing costs, and before regulating. So much has been added into the code that cost increases and complexity have become overwhelming.

CHBA is actively driving innovation within the sector. We’re engaged in the pursuit of affordable solutions through our CHBA Net Zero Energy Home Labelling Program, which has labelled over 3600 homes built by CHBA members across the country to-date. CHBA is innovating in many other areas as well, such as climate change adaptation and resilience.

Another very important consideration is that today’s new homes are already very efficient. To address climate change within the sector and reduce GHG emissions, the critical target needs to be the existing housing stock through energy retrofits during home renovations. CHBA’s Net Zero Home Labelling Program includes renovations to address this need. To tackle climate change, we need to focus on the 16 million existing Canadian housing units that have emissions much higher than today’s newly built homes. The returns on marginal improved savings on new builds are a tiny fraction of what can be saved addressing the existing housing stock in a comprehensive way through energy retrofits.

GIven the expense of moving to higher levels of energy efficiency, it is important to invest in R&D to find measures that do not reduce affordability. The government should focus on neutral-cost innovation to bring down costs and scale up use first, before regulating excessively high levels of energy performance. CHBA cautions against adding even more costs through code and/or regulation that will impact housing affordability in Canada, at a time when home is more important than ever. Better solutions can be and should be found first to improve affordability for consumers, not make it worse.

CHBA is also very concerned with the development system for the National Building Code, which has changed dramatically in recent years. Driven by political policy direction and unreasonable timelines, the system has become very flawed. It is driving up prices for housing without proper due diligence, transparency, or sufficient focus on affordability and the home building process. The development system needs to be revisited, and the just-released 2025 code needs to be put on hold and revisited to make changes that reflect these issues – particularly affordability – before provincial adoption. Facing similar challenges, Australia has recently paused all changes to their national building code until 2029. Canada needs to do the same.

Recommendations:

- Pause all changes to the National Building Code (NBC), as Australia has done.

- Review the code to implement changes to reduce costs and complexity, starting with the 2025 code, and delay adoption until adjusted.

- Fix the NBC development system to better reflect the needs of housing (i.e. to address affordability, construction complexity, transparency, evidence-based decision making, industry insights, and more).

- Adopt affordability as a core objective of the NBC and all related standards.

- Establish and work with provinces to enforce a binding NBC Interpretation Centre.

- Invest in innovation and R&D for lower cost or cost-neutral solutions and do not regulate until such solutions are proven.

5. SUPPORT HOUSING AFFORDABILITY AND SUPPLY THROUGH RENOVATION MEASURES

Almost all of the issues and recommendations in this document apply to both renovation and new construction, e.g. GST removal, labour support, addressing code, etc. However, to support more housing affordability and supply, a few renovation-specific measures are recommended, including renovation tax credits, which are proven to fight the underground economy, creating a level playing field for honest businesses while increasing tax revenue for the government:

Recommendations:

- Introduce renovation tax credits for:

- First-Time Home Buyers to support their entry to homeownership and upgrading to today’s standards;

- Energy Efficiency Retrofits to meet the government’s climate change goals, because given the efficiency of new housing, it is the existing stock that is most important to tackle.

Note: A key benefit of tax credits is their successful impact on battling the underground economy. Cash operators in the renovation business cost governments millions of dollars each year, and put Canadians’ homes at risk through unscrupulous operators and sub-standard work. Putting tax credits in place makes Canadians want to secure receipts, which greatly reduces cash jobs and creates a level playing field for honest contractors. - Include Net Zero and Net Zero Ready retrofits as “substantial renovations” under the New Housing GST Rebate.The expense of moving to these very high levels of efficiency are similar to the costs of rebuilds that are eligible for the New Housing GST Rebate. Given the government’s pursuit of climate change goals, making Net Zero renovations eligible for this rebate only makes sense.

7. ADDRESS LABOUR SHORTAGES

Canada doesn’t have enough workers to meet the status quo in terms of housing starts moving forward, let alone to double them. At the same time, current layoffs are putting the industry at risk for still more industry capacity loss, and on a permanent basis as laid-off workers leave the sector. On top of that, BuildForce Canada estimates that 22% of the residential construction labour force will retire over the next decade.

Current government funding and programming does not adequately or properly address residential construction’s workforce challenges. It is important to remember that the home building sector is:

- Different from the industrial, commercial, and institutional construction (ICI) sector and has entirely separate needs.

- Largely made up of SMEs – many are microbusinesses with less than 5 employees.

- Largely not unionized (outside of the GTA and Quebec).

- Not adequately supported by the apprenticeship system.

To address the workforce challenges facing residential construction, CHBA’s recommendations are based on three pillars: 1) growing the domestic workforce; 2) updating the immigration system; and 3) supporting increased productivity.

Growing the domestic workforce

The government should do everything possible to encourage more Canadians to consider a careers in the skilled trades, and support the apprenticeship system as well as the non-apprenticeship pathways common in residential construction to help those interested to pursue skilled careers in home building and renovation. There is significant opportunity to encourage groups traditionally underrepresented in the current construction labour force, including women, Indigenous people, and new Canadians. As a country, we need leadership to demonstrate these are good and valued careers, and we need to support the people who work in them or seek to. The Canadian Home Builders’ Association is doing its part to promote the skilled trades and provide information to those looking to begin a career in residential construction. Visit our website for more information.

Recommendations:

- Update the National Occupation Classification System to properly reflect occupations in residential construction (and reflect the differences between residential and non-residential construction) to enable government funding to properly flow to support residential trades and enable the immigration system to bring in the right workers to build and renovate Canada’s homes.

- Work with CHBA (and other stakeholders) to redevelop the education, training and certification system for skilled workers in residential construction to properly reflect the realities of this part of the sector.

Updating the immigration system

While Canada has reduced its immigration volume, it is critical that the immigrants that Canada does continue to bring in are aligned with the needs of the economy, therefore better targeting of those that can join the residential construction industry is essential. Robust immigration pathways do not yet exist to bring in the actual people that are needed to double housing starts, but it’s imperative those pathways are created in order to address residential construction workforce shortages and build the homes needed to restore affordability.

CHBA understands that these recommendations represent a significant shift for Canada’s immigration system. For too long, these changes have been avoided, but now they’re critical to meet Canada’s housing supply needs. Canada must target entrants with the right competencies, transferable experience, and desire to build a career in the sector.

Recommendations:

- With an updated NOC system (above), enhance category-based selection for Express Entry to support the specifics of the residential construction sector, including bringing in TEERs 3, 4, and 5 workers, such as installers, framers, and general labourers and helpers, and factory-built construction workers (which tend to be classified as “manufacturing” roles and are often overlooked).

Supporting increased productivity

Increasing productivity in the industry is certainly an important part of addressing the lack of skilled labour to build homes. Supporting the industry in its shift towards factory-built construction offers many benefits, but it’s not a magic bullet answer. There are very real business risks and systemic barriers that have prevented the industry from transitioning to more factory-built construction.

The site-built housing industry has evolved to successfully weather the continual boom and bust cycles of the housing market by keeping keeping overhead low. Conversely, factory-built construction requires high capital investment, high overhead, a steady workforce, and steady demand/throughput, which means it’s not inherently well suited to boom and bust cycles. Costly up-front capital needed to invest in modular and other factory-built technologies means it’s a solution that requires government support in both policy and programming in order to be widely adopted. Just as the federal government is supporting innovation in clean energy, so too should it invest in necessary solutions to help alleviate Canada’s chronic housing shortage.

The Canadian Home Builders’ Association recognized the critical role of increased productivity within the sector, establishing its Modular Construction Council back in 2017. Through that, we developed a Sector Transition Strategy to explain the current situation, the challenges and opportunities, and provide recommendations to get Canada using more factory-built construction.

Recommendations:

- Continue to implement recommendations from CHBA’s Sector Transition Strategy, including:

- Financial system, regulatory and policy support from all levels of government to create a conducive business environment.

- Targeted programming for the transition for factories and builders.

- Strategic funding to de-risk investments and support modular construction financing.

- Investment tax credits to accelerate equipment and systems investment.

- Invest in CHBA’s proposed Factory-Built Construction Hub for:

- information and training for builders and building officials; post-secondary programs; addressing regulatory barriers; innovation in factory-built systems.

Next Steps

Housing affordability and housing supply are intrinsically tied, and both are complex issues, but as you can see, there are tangible things the federal government can do to improve the challenges that Canadians are facing.

And while there is a lot of information out there on how affordability works, not all of it is accurate. Explore this website for information about what impacts housing affordability in Canada.