When Canadians talk about housing affordability, the conversation often focuses on interest rates, land prices, or construction costs. But there’s another big contributor: development charges (DCs), which are municipal taxes that are embedded in the price of every new home. These taxes directly impact the cost to build new homes, quietly pushing homeownership in many cities further out of reach and stifling new housing supply at a time when Canada must nearly double housing starts to address affordability, especially for homeownership.

What are development charges (DCs)?

DCs are upfront fees municipalities levy on new residential construction. They are initially paid by developers for each new unit they build before shovels even hit the ground, but the costs ultimately are borne by the end home buyer as part of the final purchase price of a new home.

From growth-related fees to a hidden tax on new housing

In theory, DCs are meant to cover the proportionate cost of growth-related infrastructure such as new roads, water and sewer connections, and community services required to support new neighbourhoods. In practice, however, they have expanded far beyond that original purpose.

Over time, DCs have increasingly been used to fund infrastructure and amenities that benefit the broader, existing community, not just new developments. Aging infrastructure in older neighbourhoods, expanded road networks, and other municipal systems that should be funded through general revenues are instead being loaded onto new housing because raising property taxes is a politically unpopular move.

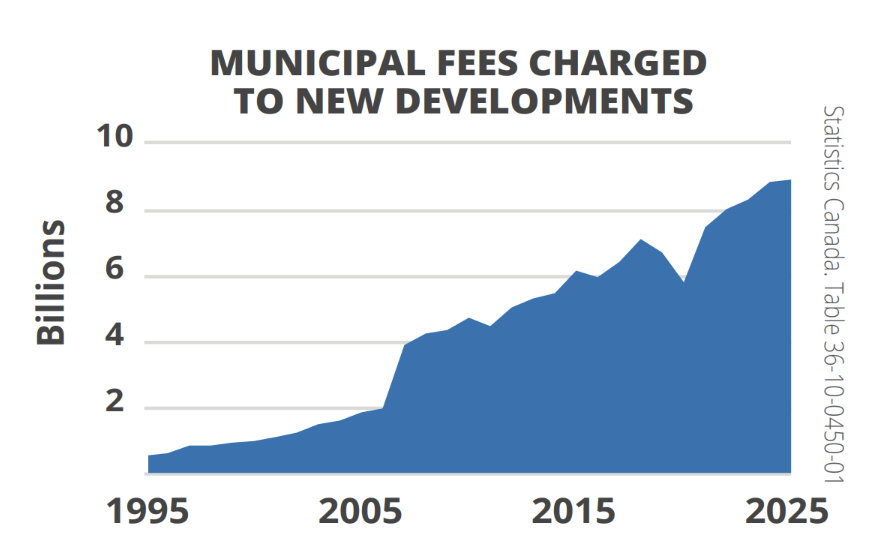

DCs are rising far faster than inflation

While it’s true that costs increase over time, the scale of DC growth in Canada has not been because of inflation – it has been through expanding the list of things that buyers of new homes have to pay; things that buyers of homes in the past never had to fund (and things that in municipalities with better policies today still fund by other means).

CHBA’s Municipal Benchmarking Study reveals that DCs have grown to unsustainable levels – to nearly $200,000 on a typical home in the Greater Toronto Area and almost $100,000 in the Greater Vancouver Area.

These are not marginal costs: they are huge sums of money in the form of taxation that can mean the difference between qualifying for a mortgage or being locked out of homeownership altogether.

An unfair burden on new home buyers

Municipalities often justify rising DCs with the argument that “growth should pay for growth,” and that “developers should pay.” But developers don’t absorb these costs: buyers do. And in many cases, these development taxes are being pooled into the municipality’s larger budget, which means they can pay for things other than the development of the new community, like aging infrastructure in older neighbourhoods. In many cases, the charges have been so excessive that they are sitting in unused municipal surplus funds.

This creates a fundamental fairness issue. New buyers, who are often younger Canadians trying to enter the housing market, are shouldering DCs to a level that previous generations of homeowners never faced. The issue compounds when we know that land development improves the desirability to live in different communities overall, meaning that existing homeowners benefit from the DCs paid by new homeowners in the form of greater amenities and increased home valuations.

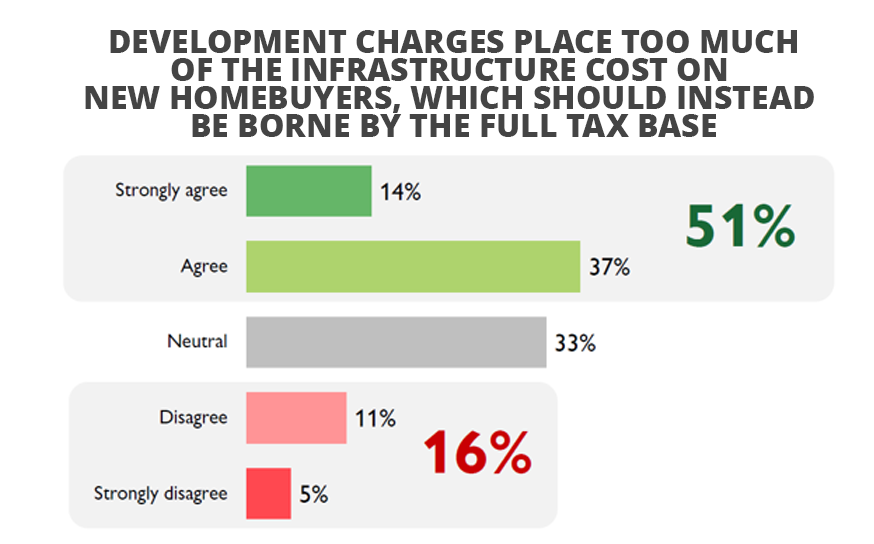

Most Canadians recognize this injustice and as this issue has become more public, they want to see action. Public opinion data from Abacus Data reveals that 51% of Canadians agree development charges place too much of the cost of infrastructure on new home buyers and that the costs should be shared across the broader tax base. Only 16 percent disagree.

Why this matters for housing supply

Exorbitant development charges don’t just affect the pocketbooks of buyers of new homes: they affect the creation of new housing supply. When the cost of building becomes prohibitive, projects stall or are cancelled, reducing the number of homes being built. That, in turn, worsens housing shortages and drives prices even higher.

CHBA recommendations for addressing DCs

Everyone benefits from growth, and everyone should contribute their fair share. The federal government has a role to play in fixing this system, and CHBA has solutions. As such, CHBA recommends that the federal government:

- Continue pressure through all means to ensure municipalities reduce DCs. This should be done through requirements in funding transfers for infrastructure and transit, and through the Housing Accelerator Fund and Housing Infrastructure Fund.

- Follow through on its commitment to offset development charges.

- Work with provinces and municipalities to mandate that alternatives to DCs be found (see below for some ideas).

- Maintain and increase housing supportive infrastructure and transit investments and tie them to housing affordability and supply outcomes. (e.g., increased density, reduced parking minimums, etc.)

There are fairer alternatives

CHBA agrees that growth needs infrastructure, but how it’s paid for, and by whom, matters. As currently structured, DCs in many cities are neither fair nor sustainable. Yet many municipalities have come to rely on them to fund infrastructure improvements.

Better, fairer alternatives to DCs must be explored to lower the cost of new housing. That’s why CHBA recommends that federal government mandate alternatives be found. Several exist, as demonstrated in other countries and from right here in Canada, including:

- Municipal debt financing: Infrastructure should be financed through long-term borrowing and repaid over 20-30 years, spreading costs more equitably. Québec follows this approach – DCs are not systematically applied but are instead funded through the general tax base for the most part. This results in lower fees and comparatively lower housing prices.

- User charges: Costs for water, wastewater, or roads can be recovered through user charges, reflecting actual usage rather than disproportionately penalizing new home buyers.

- Senior government support: A more robust system of federal/provincial grants or revenue sharing would help fund infrastructure without distorting housing prices. This, in tandem with updated provincial development tax legislation, would go a long way toward supporting the creation of new housing.

- Land value capture techniques: When public investments increase land values, a portion of that gain can be recaptured to fund infrastructure. This ensures benefits are shared rather than over-taxing new homes.

- Community Development Districts (CDDs): CDDs are local government entities that issue bonds to finance the building, operation, and maintenance of community infrastructure like streetlights, parks, sidewalks, and more. These are repaid through assessments charged to property owners within the CDD, shifting infrastructure costs away from municipalities and in turn, buyers of new homes.

- Shifting some charges to property taxes: This should be done for services that benefit the wider community beyond new development, such as libraries, roads, and new fire stations. Modest increases spread across many existing properties can raise significant revenue, instead of imposing massive fees on a small number of new home buyers.

Overall, if Canada is serious about restoring housing affordability, municipalities must rethink their reliance on excessive development charges and adopt fairer, more transparent ways to fund growth. Continuing down the current path only deepens the housing crisis and locks more Canadians out of the dream of homeownership.

For more of CHBA’s recommendations on how the federal government can help solve the housing supply and affordability crisis, visit How the government can help unlock the door to homeownership.